The fourth quarter provided a strong reassurance that markets can still deliver impressive returns in all major asset classes. Both equities and bonds delivered returns in the neighbourhood of 8% in the final quarter of the year, pushing annual returns to levels that hopefully will make investors forget about the dreadful market returns of 2022!

Once again, the experience of markets has defied the predictions of just about everyone who claims to be some kind of expert predictor. The only thing that seems to be predictable in investing is human behaviour! Sadly, there is so much noise being created in the press, on television, and on social media platforms, it is hard to stay focused on what matters or actually works. Investment companies that spend heavily on advertising try to appeal to your emotions, not reality. As many of you are probably aware, Justwealth does not engage in such shameless practices.

Following the weak calendar year returns in 2022, we spent much of the first half of the year convincing clients and others NOT to switch their investments to GICs or other safe, guaranteed investments (unless of course they had a short-term time horizon) since it was very likely not in their best interest. Our unrelenting push to educate peaked in July when we published our most-read-ever blog post: GICs: The Worst Investment Ever?. At the same time, banks and other firms that profit enormously from selling GICs were promoting GICs as a great investment. One of these opinions is biased and conflicted, the other is based on analysis and evidence and in a client’s best interest…

So how did this play out in 2023? Well, investors that locked themselves into GICs near the beginning of the year might have earned 4%, perhaps a bit more, finishing BELOW the return of every one of Justwealth’s portfolio returns in 2023. While we would be the first to point out that you should not focus on short-term results, most people who chose to invest in GICs engaged in short-term decision making, choosing fear over rationality. The evidence is overwhelmingly bad for GICs vs. any other investment option.

As market returns improved throughout the course of the year, enthusiasm picked up for greater risk in investing, perhaps propelling markets to become a little over-inflated. Momentum shifts in investing can happen quickly and with great force, often going too far before some kind of reversal happens. The extremely strong performance of both bonds and equities in the fourth quarter makes us a bit nervous that investors’ expectations are getting a little too aggressive, or in other words, greed has replaced fear.

Greed and fear can be equally damaging to one’s wealth when they drive decision making over sensibility and rationality. To make a driving analogy, greed is pushing the accelerator to the floor, and fear is slamming on the brakes. Both can cause bad accidents. Our suggestion is always to lock in the cruise control at a steady speed that you are comfortable with.

Looking forward to 2024, we believe that the focus and emphasis on inflation data will fade. The steady-but-slow progress that has been made makes inflation a smaller risk, and with restrictive monetary policy still firmly in place, it seems very unlikely that inflation will come roaring back. Whether inflation returns to the targeted 2% or just continues to get closer to it in 2024 is not really that relevant.

What we do believe to be relevant in 2024 will be the strength of economic growth. In the face of an onslaught of interest rate hikes, the economies of Canada and the U.S. have remained remarkably resilient. This may continue, albeit at a modestly lower growth rate, or it may come crashing down as has been predicted by some for close to 2 years now.

In the first scenario of lower, but positive, growth, equities could continue to perform well, but below the lofty levels experienced in 2023. Bonds, however, may struggle a bit as a number of interest rate cuts have been priced into markets. If the economy remains strong, there is little incentive to lower rates while inflation is still too high, so bond returns may be somewhat pressured, but still potentially positive since yields are relatively high.

In the second scenario, the onset of a recession is typically not good for profits, so arguably not good for equities as investors will predictably panic. As panic peaks, central banks have historically come to the rescue – not for equity investors – but to avoid deflation, which is one of their responsibilities. Yes, this can happen quickly and as fast as rates went up recently, they can come down even quicker, providing rapid relief to equity performance and boosting bond performance to above-average levels.

Of course, these aren’t the only two possible outcomes, but if they were, then equity returns could be anywhere from good to really bad, but bond returns should be stable to above average. We have been saying for some time that bond returns have not looked this promising for possibly a decade or longer, and that still holds true even after the strong finish in 2023.

As Justwealth enters its ninth year of managing the wealth of a wide range of Canadian investors, we are very proud of the investment counselling that we have provided, based on sound, evidence-based principles. Furthermore, our performance track record demonstrates that Justwealth has delivered best-in-class performance for our deserving clients, whether you compare us to other robo-advisors, bank mutual fund managed portfolios, or packaged all-in-one ETFs (all data is available upon request).

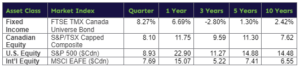

Here is a recap of market performance as of December 31, 2023*

* Source: Morningstar Direct. Performance annualized for periods greater than 1 year.

Comments are closed.