A divergence in economic prosperity may be firmly unfolding between Canada and the United States. Recent statistics show that employment data in Canada is showing clear signs of weakening from the punishing interest rates which started their ascent back in early 2022. As recently as July of 2022, unemployment in Canada was at 4.9%. This number has now jumped to 6.1%. In contrast, unemployment in the United States in July 2022 was at 3.5% and has only modestly increased to 3.8%. Similarly, Canadian GDP has been hovering near 0% GDP growth for almost 2 years, whereas U.S. GDP continues to chug along at a rate of 2.5% or higher over the same time period.

Perhaps the most puzzling data though, is that inflation remains stubbornly above the targeted 2% rate in both countries!

As we outlined in our 1Q 2023 Market Commentary, inflation cannot be brought back down to normal until some serious economic pain has been inflicted on businesses and consumers. One year later, this has still not fully materialized, but we seem to be getting much closer to that point in Canada, compared to the United States. The currency markets seem to be paying attention to the divergence as well, as the Canadian dollar is hovering near its lowest point relative to the U.S. dollar going back to 2020.

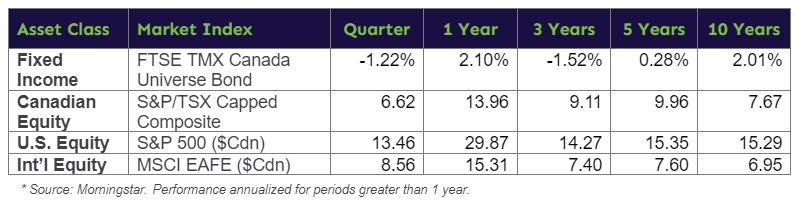

When it comes to stock markets, both Canada and the United States posted strong returns in the first quarter, with Canada rising 6.62% and the U.S. moving up by a currency-assisted 13.46%. International markets also enjoyed success by gaining 8.56%. Overall, that is a very strong quarter, and puts one-year returns at very impressive double-digit returns.

A popular soundbite in the media these days is that “rates will be higher for longer”. Funny, not many were saying that 3 months ago after bonds had a massive one-quarter rally and that rate cuts seemed “imminent”. As per our cautionary comments in our 4Q 2023 Market Commentary, however, bond markets did indeed get a bit ahead of themselves and fell by 1.22% this past quarter.

We have kept duration (interest rate sensitivity) low in the fixed income components of our portfolios since our inception in 2016, and that has allowed us to generate returns substantially better than standard bond market returns. This is sometimes overlooked when simply looking at individual holding returns so we remind our investors that returns should be judged at an account or portfolio level, not individual holdings. The time will come when interest rates go back down, and those holdings that suffered the most when interest rates went up will perform best when rates go down.

Our performance relative to peers remains very strong compared to most other risk-comparable investment options in Canada. Since we first started comparing Justwealth performance relative to asset allocation products offered by Canada’s big banks, Justwealth has consistently demonstrated outperformance of 2-3% or more per year at all levels of the risk spectrum. That is a STAGGERING difference, and it’s not like banks are known for their outstanding customer service! Banks and their subsidiaries have done little to deserve your investing business, so please spread the word and share this link with your friends, family members and colleagues: https://www.justwealth.com/banks/.

Thanks for your continued support!

Here is a recap of market performance as of March 31, 2024*

Comments are closed.